Cryptocurrency Prices by Coinlib

How a lot of your portfolio ought to truly be in crypto?

TL;DR: The 5–10% rule is a place to begin, not a solution. The best crypto allocation will depend on three variables: your liquidity place outdoors crypto, your current asset combine, and your time horizon. Work by these three questions earlier than evaluating any numbers. Should you maintain crypto on a platform like Nexo that enables borrowing in opposition to your place, the efficient liquidity of a bigger allocation modifications too.

Begin with the query behind the query

Earlier than sizing a crypto allocation, get clear on what you are attempting to do with it.

Most holders purchase for considered one of 4 causes: long-term appreciation, inflation safety, energetic use (borrowing in opposition to holdings, incomes yield), or hypothesis. The best allocation is completely different for every. A protracted-term appreciation thesis helps a bigger, affected person place. A speculative thesis helps a smaller one you are genuinely ready to lose. Should you're utilizing crypto actively, borrowing in opposition to it by a credit line or earning daily interest, the asset is doing extra work than if it is sitting in a pockets. That modifications the way you worth holding extra of it.

Getting clear in your motive is the primary resolution. All the pieces else follows.

The three-question framework

Query 1: What's your liquidity place outdoors crypto?

That is the variable most allocation guides skip fully.

If in case you have 12 months of dwelling bills in a checking account and a secure revenue, you possibly can maintain a unstable asset by a major drawdown with out being compelled to promote on the worst time. That cushion helps a bigger allocation.

In case your emergency fund is skinny or your revenue is variable, a big crypto place creates a selected danger: you could have to promote throughout a downturn to cowl one thing else. Promoting underneath stress somewhat than by alternative is how most retail holders lock in losses they did not have to take.

A sensible threshold: crypto shouldn't signify extra of your portfolio than you can afford to see fall 70% with out altering anything about your monetary life. Bitcoin fell 83% from its November 2021 peak of $69,000 to its November 2022 low of $15,500. Ethereum fell 81% over the identical interval. These will not be edge instances. They're the historic norm for main crypto belongings in bear markets. If that state of affairs would imply you possibly can't cowl necessities, the allocation is simply too giant.

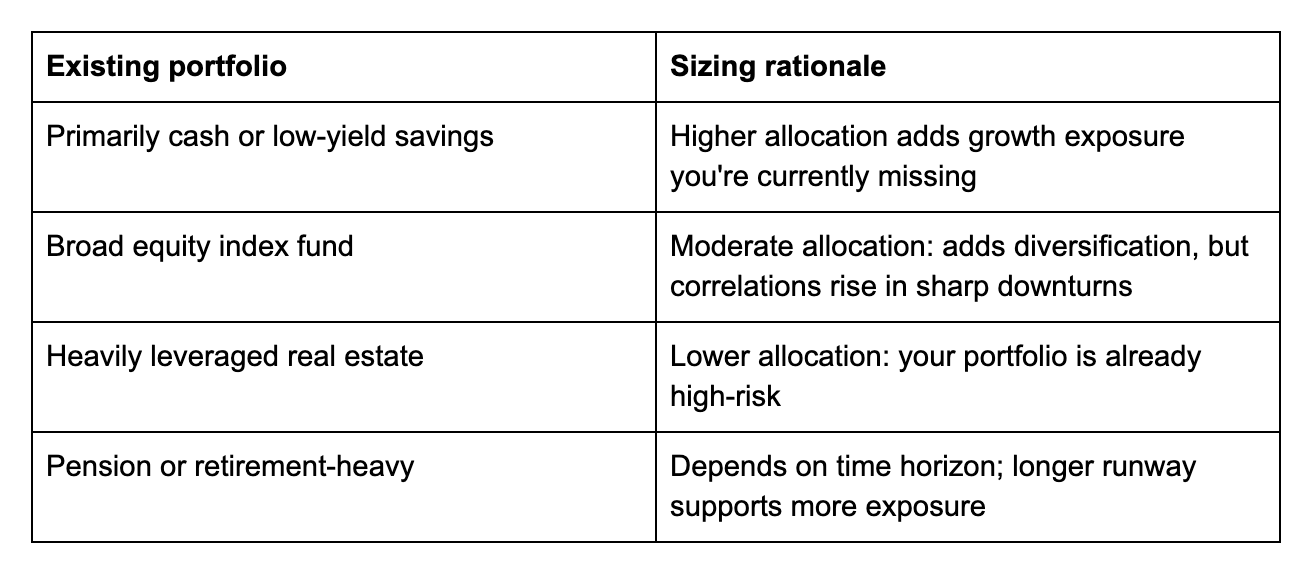

Query 2: What does your current asset combine seem like?

Crypto does not exist in isolation. It interacts with every thing else you personal.

Query 3: What's your time horizon?

Crypto's volatility is most damaging over quick time horizons. Should you want the cash in two years, a drawdown that takes three years to get well is an actual drawback. In case your horizon is ten years, that very same drawdown is noise. Each four-year rolling interval in Bitcoin's historical past since 2013 has closed larger than it opened, a knowledge level price holding in thoughts when calibrating how a lot volatility you possibly can afford to disregard.

A tough adjustment to your base allocation:

Beneath 3 years: 5% or much less, or stablecoins solely

3–7 years: 5–15% relying on liquidity and asset combine

7+ years: as much as 20–25% is defensible for traders with robust liquidity and a real long-term thesis

How borrowing modifications the calculation

One issue most allocation frameworks ignore: for those who maintain crypto on a platform like Nexo, your place is not only a passive wager. It is an asset you possibly can borrow in opposition to.

Should you want liquidity and do not need to promote, a crypto-backed credit line allows you to entry funds utilizing your Bitcoin or Ethereum as collateral, from 2.9% annual curiosity for eligible shoppers. Your holdings keep in place. If the worth recovers, your full place advantages. Technique (previously MicroStrategy), which held roughly 528,185 BTC as of April 2026, has used a model of this logic at an institutional scale, borrowing in opposition to Bitcoin reserves somewhat than liquidating them to fund operations.

This doesn't suggest holding greater than your monetary scenario helps. But it surely does imply that for long-term holders, the provision of borrowing will increase the efficient liquidity of the asset, which modifications the sensible danger of a bigger allocation.

Equally, for those who're earning daily interest in your holdings, the place generates yield when you maintain. That compounds the case for sizing the allocation intentionally somewhat than defaulting to the smallest snug quantity.

What most individuals get mistaken

The most typical mistake is not holding an excessive amount of crypto. It is holding greater than their liquidity place can soak up with out forcing a sale on the mistaken time.

The second is treating 5–10% as a ceiling for everybody. For a 30-year-old with a secure revenue, a full emergency fund, and a 10-year horizon, that vary could also be conservative. For somebody 5 years from retirement with modest financial savings, it might be too excessive.

The third shouldn't be revisiting the allocation as circumstances change. A ten% place that made sense at €50,000 represents a unique quantity, and a unique psychological actuality, at €200,000.

Discover crypto financial savings and borrowing on Nexo

As soon as you've got sized your allocation, placing it to work issues as a lot as how a lot you maintain. Flexible Savings earns each day curiosity on crypto and stablecoins with no lock-up. Fixed-term Savings affords larger charges for dedicated durations. And for those who ever want liquidity with out promoting, Nexo's crypto-backed credit line provides you entry to funds from 1.9% annual curiosity.

Often requested questions

1. How a lot of my portfolio ought to be in crypto? It will depend on your liquidity place, current asset combine, and time horizon. The 5–10% rule is a place to begin, not a ceiling or a ground. Work by the three questions above to reach at a quantity that matches your scenario.

2. Is 10% crypto an excessive amount of? For some folks, sure. For others, no. If 10% falling 70% would pressure you to promote or change your monetary behaviour, it is an excessive amount of. If it would not, 10% could also be conservative relying in your time horizon and circumstances.

3. Does borrowing in opposition to crypto change how a lot I ought to maintain? It may. Should you maintain crypto on a platform that enables borrowing in opposition to your place, the asset has larger efficient liquidity than one you possibly can solely entry by promoting. That modifications the sensible danger of holding a bigger allocation.

4. How usually ought to I rebalance? A sensible set off is when your crypto allocation has moved greater than 5 proportion factors out of your goal as a consequence of value actions. Rising costs that push crypto from 10% to 18% of your portfolio could warrant trimming again. Falling costs that push it to five% could warrant topping up, in case your thesis is unchanged.