Cryptocurrency Prices by Coinlib

Markets At the moment – Could 13, 2026

Each day evaluation of crypto markets and the forces shaping them, from the Nexo analysis desk.

Bitcoin retains its positive aspects regardless of sizzling U.S. inflation

Bitcoin is holding above $80,000 and the entire crypto market cap is edging again towards $2.7 trillion, regardless of U.S. inflation accelerating in April. Yesterday's CPI printed at 3.8% y/y, with power contributing 40% of the rise and pushing December rate-hike odds to almost 30%, up from 15% every week in the past. The cross-asset response is blended: U.S. fairness futures are decrease alongside Asian and European indices, whereas Brent crude holds regular close to $106 a barrel. Gold has stabilized round $4,700 however is down 3% over the previous month and almost 11% under its February file. The principle query for markets now could be how central banks reply to firmer inflation.

Bitcoin

Bitcoin is buying and selling close to $81,000, down 0.3% on the day, with the 7-day vary compressed to roughly $79,500–$82,500. Per Glassnode, BTC perpetual open curiosity has fallen 7% from every week in the past to $36.8 billion, in step with deleveraging on the transfer under $80,000. Funding sits at 3.4% annualized after averaging barely detrimental over the previous 30 days, indicating balanced positioning relatively than crowded lengthy.

Choices markets line up the identical manner. Implied volatility has compressed, with the time period construction in regular contango: one-week ATM IV at 35.4%, one-month at 36.2%, three-month at 38.7%, and six-month at 41.8%. The volatility setup displays pricing for a contained near-term transfer. A clear break above $82,500 or under $79,500 would doubtless reset each volatility and positioning. The catalyst is extra prone to come from charges pricing than from crypto-native flows.

Ethereum & Altcoins

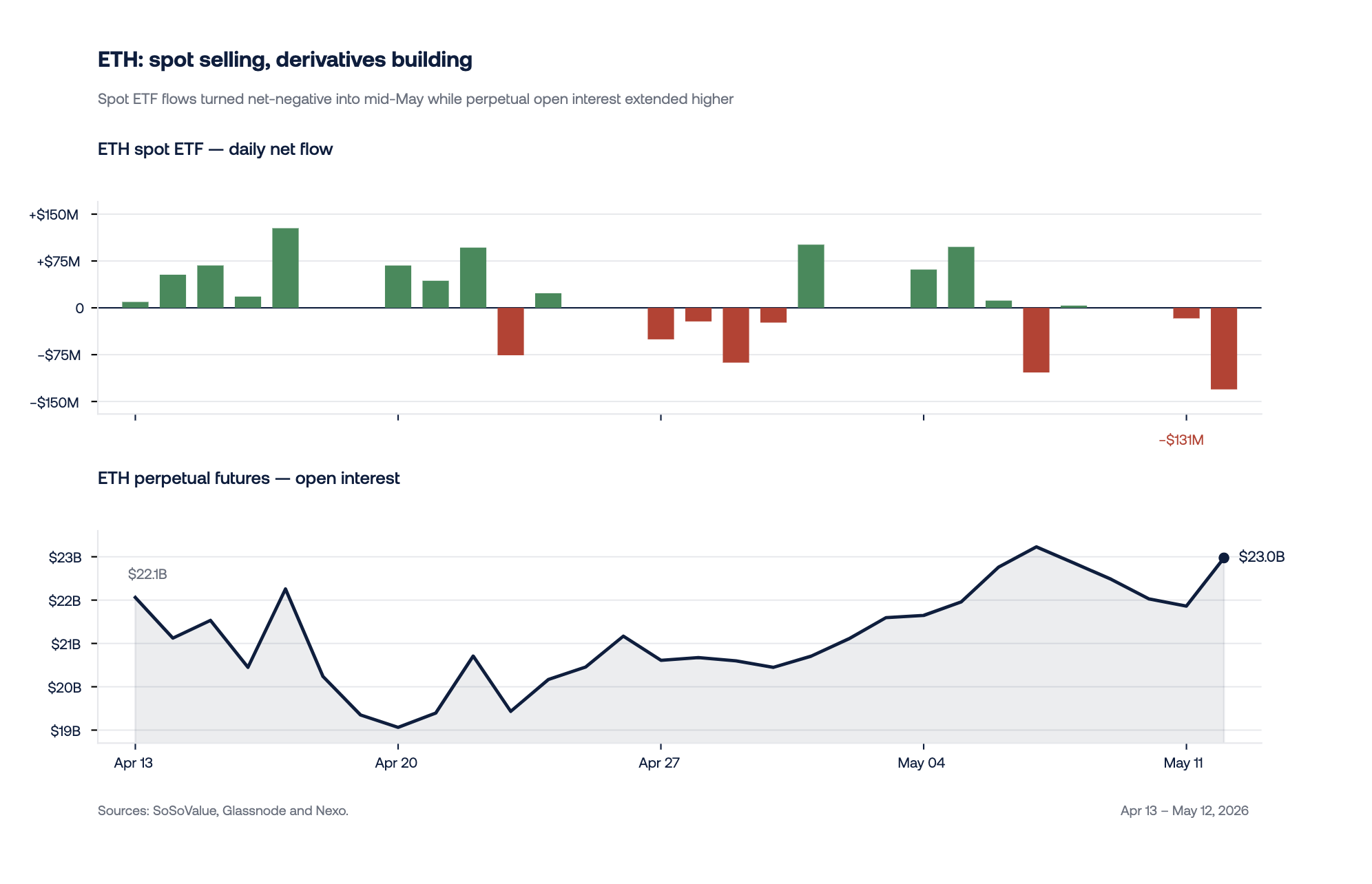

Ethereum is buying and selling close to $2,300, flat on the day and down 3% on the week. Spot has been a web vendor all month and ETF outflows have accelerated this week. Could 12 alone noticed $131 million pulled, with the final two periods netting roughly $148 million. Derivatives, nonetheless, are pulling the opposite manner: perpetual futures open curiosity is constructing and funding has flipped constructive, with leveraged merchants including bullish publicity whilst money markets distribute.

The image in different massive altcoins is cleaner. Solana and XRP are each larger on the week, with SOL futures open curiosity up 42% over 30 days and XRP up 22%. Funding on each is persistently constructive, and spot ETFs are seeing constant inflows in Could. The institutional altcoin bid is selective: current in SOL and XRP, absent in ETH. In each circumstances real-money flows and leveraged positioning are pulling the identical manner, in contrast to ETH, the place leveraged size is constructing right into a money market that is promoting.

Macro & Institutional

December Brent futures are again above $90 a barrel after U.S. President Trump labeled Tehran's newest peace overture “rubbish”, the clearest sign but that the Hormuz premium is sticking. A sustained transfer larger in oil would harden the pass-through CPI breadth confirmed yesterday. Two-year Treasury yields at 4% and rising odds of a December Fed fee hike tilt the implied coverage path hawkish, narrowing the easing markets had priced via Q1.

China is doubtlessly the offsetting drive within the world threat image. April exports rose 14% year-on-year towards ~8% consensus, with know-how main regardless of chip restrictions. The CSI 300, China's blue-chip fairness benchmark, sits above its prior Trump 1.0 peak; 10-year CGB yields commerce under 2%. Resilient progress and accommodative financial circumstances stand in sharp distinction to US repricing. The Trump-Xi summit is the binary swing issue: with rare-earths leverage and AI deployment capability, Beijing arrives in a materially stronger place than in 2017. A constructive summit retains threat supported; escalation exposes it to one-sided Fed strain.

On the institutional facet, the Senate confirmed Kevin Warsh to the Federal Reserve Board and chair affirmation is broadly anticipated. The Powell-to-Warsh transition completes towards an inflation regime wherein the room for a dovish pivot has narrowed materially.

Trying Forward

Fed's Collins and Kashkari ship the primary Fed remarks since April CPI, adopted later within the session by ECB's Lagarde — early sign on how central financial institution response capabilities are recalibrating to the print. The US 30-12 months Treasury public sale prints between the 2 Fed appearances, testing long-end demand after yesterday's comfortable 10-12 months. Focus on the finish of the week shifts to US Retail Gross sales, Import Costs, and Preliminary Jobless Claims, with the Atlanta Fed's subsequent Q2 GDPNow replace to comply with. If Retail Gross sales and Import Costs reinforce CPI's broader inflation sign, the implied coverage path tilts extra hawkish; softer exercise towards agency costs reopens the stagflation body.

Creator: Dessislava Ianeva, Analyst at Nexo’s Dispatch

This materials is produced by Nexo for informational functions solely and doesn't represent monetary, funding, authorized, or tax recommendation, or a advice to transact in any digital asset. Views are the writer's as of the date of publication and should change with out discover. Data is from sources believed dependable, however Nexo makes no guarantee as to its accuracy and accepts no legal responsibility for any loss arising from reliance on this materials.