Cryptocurrency Prices by Coinlib

The nice wealth switch and crypto

Someplace between $84 trillion and $124 trillion is shifting steadily, as the biggest intergenerational asset shift in recorded historical past performs out over the subsequent twenty years.

Child Boomers and the Silent Era constructed their wealth via conventional means: actual property, equities, and pension methods. As they start to go it down, the technology receiving it thinks about cash in another way.

That distinction is structural. It has vital implications for what wealth seems like going ahead.

What's the Nice Wealth Switch?

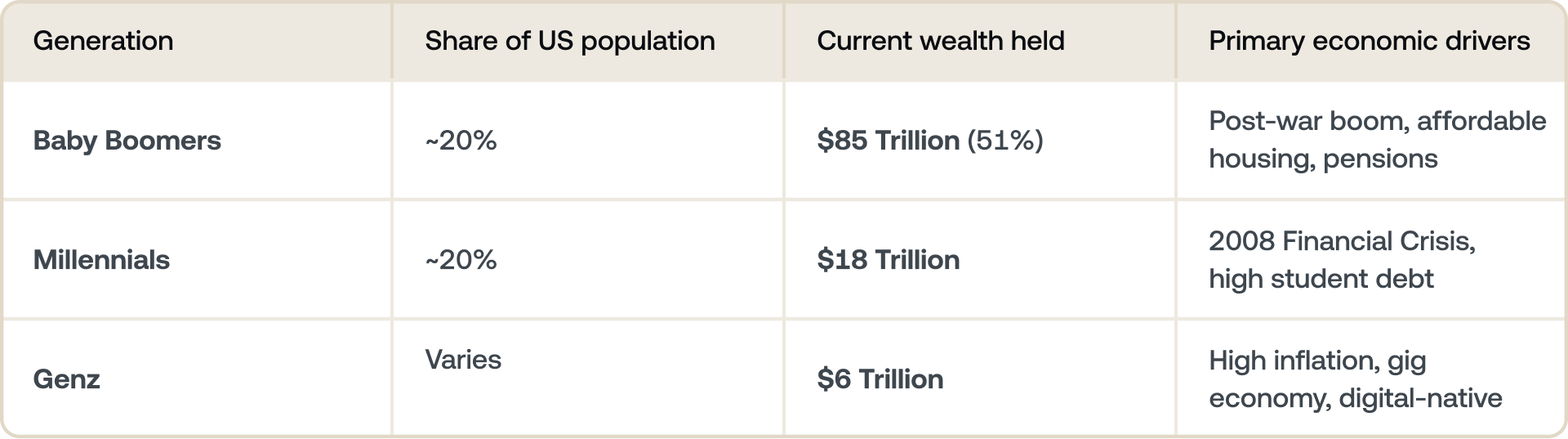

The Nice Wealth Switch is the identify given to the biggest intergenerational motion of property in recorded historical past. As Child Boomers (born between 1946 and 1964) age, the wealth they amassed over a long time is shifting to their kids and grandchildren: primarily Gen X, Millennials, and Gen Z.

It appears like a monetary planning idea. It is really a civilizational occasion.

Child Boomers benefited from a near-perfect set of financial situations. They entered the workforce throughout an extended post-war increase, purchased properties earlier than costs turned structurally unaffordable, held jobs with defined-benefit pensions, and invested in equities via one of many longest bull markets in historical past.

Immediately, the wealth hole between generations is stark:

However that hole is now starting to shut—not via wage development or coverage change, however via inheritance. The property Boomers constructed are starting to circulate downward, and the size of what is shifting is genuinely troublesome to understand.

A few of it arrives as direct inheritance. Some arrive as items, trusts, co-signed mortgages, instructional help, and enterprise capital. All of it provides as much as a generational reset of who holds what.

Why does it matter past household funds? As a result of wealth shapes markets. When a technology inherits trillions, the property they select to carry turn out to be the property that outline the subsequent period of investing. Actual property, equities, bonds, and pension funds have been the automobiles of the Boomer period. The technology now inheriting their wealth has completely different instincts—and completely different infrastructure out there to behave on them.

The dimensions of what is taking place

The numbers connected to the Nice Wealth Switch are giant sufficient to be troublesome to course of. To place it in perspective, your entire US GDP sits at roughly $28 trillion. The switch already underway dwarfs it a number of occasions over:

- $124 Trillion: The whole property projected by Cerulli Associates to alter fingers by 2048.

- $16 Trillion: The quantity set to maneuver earlier than 2033 alone.

- $54 Trillion: The quantity that can transfer intragenerationally to spouses first earlier than reaching youthful heirs.

The tempo is already accelerating. Between late 2019 and late 2024, Millennials' whole web value grew from $3.9 trillion to almost $16 trillion—a quadrupling in 5 years pushed by asset value development, profession development, and early inheritance flows. The transfers recorded in 2024 alone included $297.8 billion handed to 91 heirs, a 36% enhance year-on-year, in response to UBS.

Whereas Gen X leads the near-term image (with a mean inheritance age of 46 for fortunes over $5 million), Gen Z and Millennials comply with carefully within the a long time behind.

Why this technology is completely different

Each technology inherits the monetary framework of the one earlier than it. Child Boomers inherited post-war institutional belief—banks, pension funds, authorities bonds—and constructed their wealth inside that system.

Millennials and Gen Z are inheriting one thing fully completely different: a monetary system that failed them early, and a digital different that did not.

The 2008 monetary disaster hit Millennials on the worst attainable time—once they have been getting into the workforce, taking over pupil debt, and making an attempt to purchase their first properties. The establishments that have been speculated to be reliable both collapsed or required bailouts. That have completely formed a whole technology's relationship with conventional finance.

A January 2026 OKX survey of 1,000 People highlighted this huge behavioral divide:

- 74% of Child Boomers gave excessive belief scores to conventional banks.

- Solely one in 5 Millennials and Gen Z echoed that belief.

- Conversely, 40% of Gen Z and 41% of Millennials belief crypto platforms at a 7 or increased on a 10-point scale (in comparison with simply 9% of Boomers).

Youthful generations will not be merely much less trusting of banks. They're, for the primary time in fashionable historical past, extra trusting of another.

That different is crypto, and the adoption knowledge displays it:

- The Core Demographic: Millennials presently account for 57% of all crypto house owners within the US. Over half of Gen Z globally has owned or presently holds cryptocurrency.

- Speedy Development: One in 4 US adults now owns crypto, in response to the Nationwide Cryptocurrency Affiliation's 2026 State of Crypto Holders Report—a rise of 12 million holders in a single yr.

- Portfolio Dominance: Amongst Millennials, 62% report that crypto accounts for at the very least one-third of their whole wealth.

These aren't speculative positions held by early adopters ready to money out. For a big and rising portion of the wealth-receiving technology, crypto is already a core asset class sitting alongside, and typically forward of, conventional equities.

What's modified within the infrastructure

The criticism of crypto as a severe wealth-building software has traditionally rested on official issues: volatility, lack of institutional infrastructure, and regulatory uncertainty. These objections made sense in 2017. They make far much less sense in 2026.

The infrastructure that severe wealth administration requires now exists in crypto—and in a number of dimensions, it rivals what conventional finance presents. For a broader take a look at how one can method this, studying how to build wealth with crypto is a sensible start line.

1. Generational yield

On yield, the distinction with conventional finance is stark. On a platform like Nexo, property like USDC can earn up to 9.5% interest per yr, BTC up to 5.7%, and SOL up to 8%.

Start earning

2. Pledging collateral with out promoting

The liquidity mechanic is equally vital. One of many defining options of conventional wealth administration is the flexibility to borrow towards property with out promoting them. Rich households have finished this for generations, pledging shares or actual property to entry money whereas maintaining their positions intact.

Crypto-native platforms now provide the very same method. On Nexo, you'll be able to borrow towards your crypto at charges ranging from 1.9% APR, utilizing BTC, ETH, SOL, and different property as collateral, with out triggering a tax occasion or a sale. The asset stays in your portfolio, the place stays open, and the liquidity is accessible whenever you want it.

Borrow today

3. Institutional legitimacy

Past yield and liquidity, the diversification instruments that beforehand required a number of brokers, advisors, and establishments can now be managed inside a single ecosystem.

Institutional legitimacy has arrived sooner than most anticipated. Bitcoin spot ETFs are actively buying and selling within the US, with legacy giants like Goldman Sachs disclosing over $108 million in positions. Company treasury holdings of Bitcoin have turn out to be a typical boardroom dialog. Moreover, regulatory frameworks like MiCA within the EU and the advancing CLARITY Act within the US Senate are shifting the worldwide panorama towards lodging quite than prohibition. This basically modifications the danger profile of holding crypto as a long-term wealth asset.

Sign up

The wealth switch meets the wealth infrastructure

Here is the place the 2 developments converge.

The technology inheriting the Nice Wealth Switch is similar technology that already holds crypto, already trusts crypto platforms, and already makes use of crypto infrastructure to earn yield and entry liquidity.

When $124 trillion begins shifting in earnest, a good portion of it is going to circulate into ecosystems and platforms constructed on blockchain infrastructure. The rationale gained’t be due to ideology, however as a result of that is the place the recipients already reside.

This isn't a prediction about crypto costs. It is an statement about the place monetary gravity is shifting. Wealth follows the individuals who maintain it, and the individuals holding the subsequent technology of wealth have already made their preferences clear.

There's additionally a compounding impact value contemplating. Crypto property, not like actual property or pension funds, are natively digital—they switch immediately, globally, with out attorneys, probate, or geographic restriction. The generations that grew up with smartphones count on monetary infrastructure to work the way in which software program does.

What this implies if you happen to're constructing wealth right now

The Nice Wealth Switch is just not an occasion you anticipate. It is a context you'll be able to act inside now—and the infrastructure to take action has by no means been extra developed.

In the event you already maintain crypto, the query is whether or not your property are working as onerous as they may very well be. Holding BTC or ETH in a chilly pockets that generates no yield is the crypto equal of leaving money in a zero-interest checking account.

The yield infrastructure now exists to alter that:

- Versatile Financial savings: Allow you to earn on property whereas sustaining on the spot entry to them. If you wish to dig into how that works in follow, understanding how to earn interest on crypto covers the mechanics.

- Fastened-term Financial savings: Supply increased charges for capital you are comfy setting apart for an outlined interval to compound your long-term place.

Notice: Charges apply to eligible shoppers with a minimal portfolio steadiness of $5,000, and differ by asset and Nexo Loyalty Tier. Charges are topic to alter — all the time consult with the Nexo app for the charges relevant to your account.

In the event you're excited about wealth throughout an extended horizon—the sort of multi-decade wealth-building that the Nice Wealth Switch is forcing into focus—the borrow mechanic issues simply as a lot as yield.

Constructing wealth with out promoting your best-performing property is how the wealthiest households have all the time operated. Crypto infrastructure merely makes that method out there at retail scale. Reviewing the mechanics of borrowing against your Bitcoin explains how one can safely navigate it if you happen to're approaching it for the primary time.

The shift towards digital wealth does not all the time present up in a single headline, however the underlying gravity is simple.

These supplies are accessible globally, and the provision of this data doesn't represent entry to the providers described, which providers is probably not out there in sure jurisdictions. These supplies are for basic data functions solely and never supposed as monetary, authorized, tax, or funding recommendation, provide, solicitation, suggestion, or endorsement to make use of any of the Nexo Providers and will not be personalised or in any means tailor-made to mirror specific funding aims, monetary scenario, or wants. Digital property are topic to a excessive diploma of threat, together with however not restricted to risky market value dynamics, regulatory modifications, and technological developments. The previous efficiency of digital property is just not a dependable indicator of future outcomes. Digital property will not be cash or authorized tender, will not be backed by the federal government or by a central financial institution, and most would not have any underlying property, income stream, or different supply of worth. Impartial judgment primarily based on private circumstances needs to be exercised, and session with a certified skilled is really useful earlier than making any choice.