Cryptocurrency Prices by Coinlib

Why Crypto Holders Do not Promote In a Downturn

The brief model

Each market cycle, the identical sample performs out: costs drop, headlines flip grim, and a wave of retail holders panic-sells. In the meantime, a quieter group of refined buyers does one thing completely totally different. They borrow in opposition to their positions, earn yield on what they maintain, and wait.

When the restoration arrives, the wealth hole between these two teams widens completely. This is not luck—it is a calculated monetary playbook that severe wealth has utilized for many years, and it's now absolutely accessible to crypto holders.

The emotional intuition to promote throughout a market decline is totally comprehensible—and traditionally, it's nearly all the time mistaken.

When an asset drops 20%, 30%, or 40%, the logic of promoting feels hermetic within the second. You inform your self you might be stopping the bleeding, preserving your remaining capital, and timing a cleaner re-entry when the market lastly stabilizes.

Nevertheless, this short-term emotional logic fully collapses underneath structural scrutiny.

The triple penalty of panic promoting

Promoting your digital belongings throughout a downturn inflicts three distinct operational wounds in your portfolio concurrently:

- Everlasting capitulation: It converts a short lived paper drawdown right into a everlasting, irreversible monetary loss.

- Forfeiting the rebound: It fully removes you from the next restoration part, which traditionally occurs sooner than most market individuals anticipate.

- Tax liabilities: In most jurisdictions, promoting triggers a taxable disposal occasion. You might be pressured to navigate tax compliance on a degraded asset.

Word: Tax therapy varies considerably by area—all the time seek the advice of a certified tax skilled relating to your particular scenario.

The velocity and scale of crypto recoveries are routinely underestimated. As an example, Bitcoin fell 77% between November 2021 and November 2022, solely to rally and safe a significant all-time excessive of $125,071 in October 2025.

Each main crypto asset that has survived its first 5 years has efficiently recovered from its worst drawdowns. The buyers who captured these huge recoveries had been merely those who refused to liquidate on the backside.

In case your core funding thesis has basically modified, exiting is smart. But when the asset’s utility stays intact, the community is safe, and the one variable that modified is a short lived spot worth, the case for promoting is perhaps extremely weak.

What severe wealth has all the time achieved as a substitute

There's a cause why ultra-high-net-worth households do not liquidate their prime belongings when markets drop. It is not stubbornness; it’s an institutional framework identified colloquially as “Purchase, Borrow, Die.” This technique has been a cornerstone of multi-generational wealth preservation for over a century.

The operational logic is simple:

- Accumulate: You purchase high-conviction belongings with long-term appreciation potential.

- Leverage: Once you want real-world liquidity, you borrow in opposition to your belongings as a substitute of promoting them.

- Protect: The underlying asset stays in your portfolio, persevering with to compound and respect, when you repay the road of credit score over time.

Legacy establishments like JP Morgan, Constancy, and Charles Schwab routinely provide securities-based lending to personal banking purchasers for this actual function.

To place this in perspective, Financial institution of America's wealth administration division alone held over $50 billion in structured and asset-backed loans on the finish of 2022—proper in the course of one of many worst conventional market downturns in a decade. The rich weren't promoting their equities at a reduction; they had been borrowing in opposition to them.

This technique works due to a fundamental asymmetry: promoting is irreversible. When you forfeit your place at a depressed worth, you might be locked out. Borrowing preserves your optionality. You entry speedy liquidity whereas preserving your long-term upside intact.

Making use of the institutional playbook to crypto

The very same lending mechanics beforehand reserved for elite personal banking purchasers at the moment are obtainable natively throughout the crypto ecosystem—and they're considerably extra accessible.

Via platforms like Nexo, you may open a crypto-backed credit score line utilizing BTC, ETH, SOL, XRP, and different main digital belongings as collateral, with borrowing charges ranging from 1.9% curiosity per 12 months.

You obtain immediate funds with no compensation schedules or credit score checks, and your holdings are unlocked the second the road of credit score is settled.

Explore borrowing

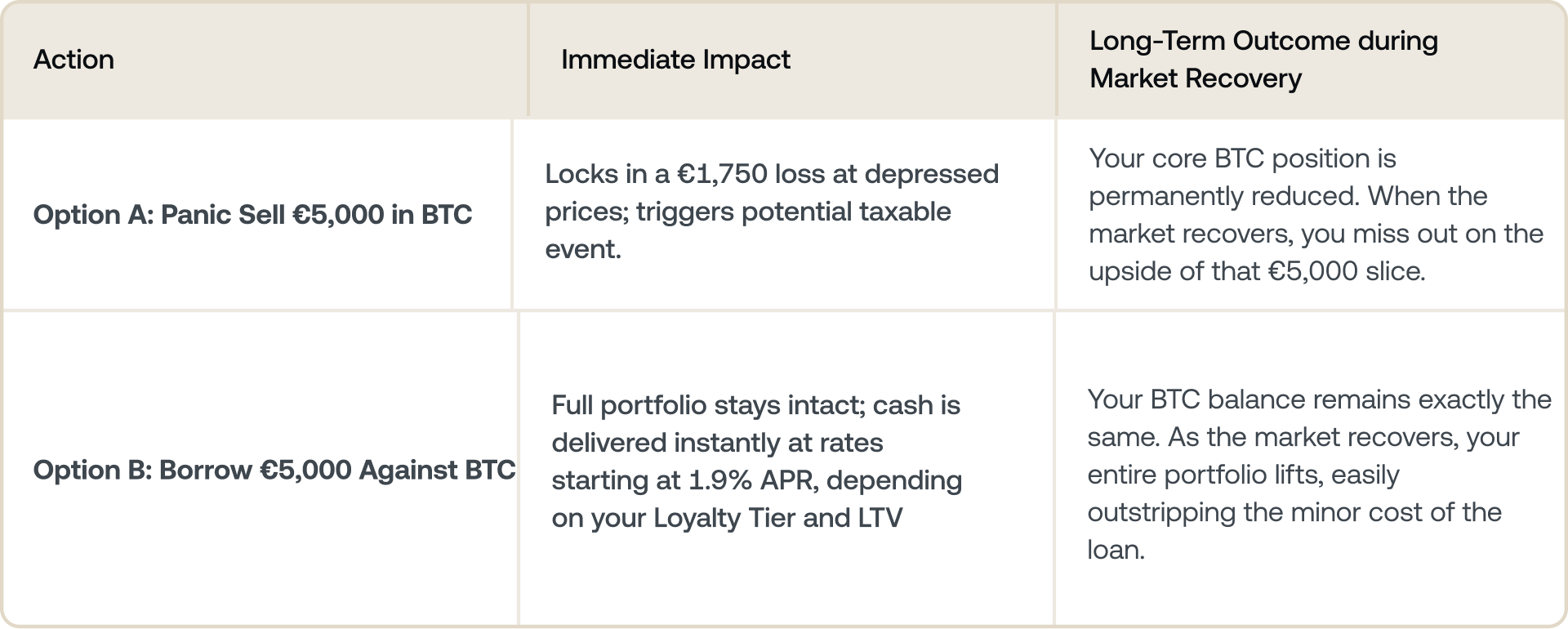

Actual-world blueprint: Promoting vs. borrowing

Think about you maintain €30,000 in BTC. The market experiences an ordinary crypto correction of 35%, quickly compressing your portfolio worth to €19,500. Out of the blue, you hit an sudden real-world expense—a €5,000 tax invoice or enterprise value.

Right here is how your selections look side-by-side:

The flip aspect: Managing your liquidation threat

Whereas borrowing lets you journey the market restoration, it isn't with out threat. As a result of crypto might be extremely risky, you have to navigate the mechanics of leverage safely:

- Understanding LTV (Mortgage-to-Worth): Once you borrow €5,000 in opposition to your remaining €19,500 in BTC, your preliminary LTV sits at round 25.6%. The upper the LTV, the riskier the mortgage.

- The Menace of Margin Calls: If BTC costs proceed to slip additional down, your LTV ratio will rise. If it hits the platform's threat threshold, you'll obtain a margin name requiring you to both add extra collateral or pay down a portion of the mortgage to stabilize your account.

- The Hazard of Liquidation: If the market drops sharply and also you fail to answer a margin name, the system will robotically liquidate (promote) a portion of your BTC at depressed costs to cowl the mortgage. This forces you into the precise state of affairs you had been making an attempt to keep away from with Possibility A: locking in everlasting losses.

Professional-Tip: Borrow Conservatively. The golden rule of crypto backing is to by no means borrow to your most restrict. Preserve a low LTV buffer so your portfolio can comfortably climate sudden market dips with out triggering a liquidation occasion.

Make your belongings work

The borrow mechanic solves the liquidity puzzle. Nevertheless, a complete bear market playbook requires a secondary part: optimization. The strategic belongings you might be not spending must be actively producing yield whereas sitting out the storm.

Leaving BTC or ETH fully idle in a chilly pockets throughout a chronic market correction is a missed alternative. Transitioning these holdings right into a high-yield atmosphere builds an automatic cushion in opposition to falling costs.

On Nexo, using Versatile Financial savings balances absolute liquidity with premium day by day payouts:

- BTC: As much as 5.7% annual curiosity

- ETH: As much as 5.25% annual curiosity

- USDC: As much as 9.5% annual curiosity

For buyers trying to quickly de-risk with out fully exiting into legacy financial institution accounts, allocating a portion of capital into dollar-pegged stablecoins like USDC or USDT is a extremely coherent technique.

Your capital stays secure, producing day by day compounding yield when you look ahead to macro circumstances to clear. Once you detect a market turnaround, you may immediately swap again into BTC or ETH proper contained in the ecosystem.

Need your portfolio to outpace market corrections? Cease holding static belongings and begin incomes day by day compounding curiosity.

Start earning

These supplies are accessible globally, and the supply of this data doesn't represent entry to the providers described, which providers is probably not obtainable in sure jurisdictions. These supplies are for common data functions solely and never meant as monetary, authorized, tax, or funding recommendation, provide, solicitation, advice, or endorsement to make use of any of the Nexo Providers and are usually not customized or in any means tailor-made to mirror explicit funding targets, monetary scenario, or wants. Digital belongings are topic to a excessive diploma of threat, together with however not restricted to risky market worth dynamics, regulatory adjustments, and technological developments. The previous efficiency of digital belongings shouldn't be a dependable indicator of future outcomes. Digital belongings are usually not cash or authorized tender, are usually not backed by the federal government or by a central financial institution, and most shouldn't have any underlying belongings, income stream, or different supply of worth. Impartial judgment based mostly on private circumstances must be exercised, and session with a certified skilled is really useful earlier than making any resolution.