Cryptocurrency Prices by Coinlib

How you can Borrow In opposition to Bitcoin

Fast reply

Sure, you may borrow towards Bitcoin with out promoting it. You pledge your BTC as collateral with a lending platform and obtain stablecoins in return. Your Bitcoin stays in your account — it is simply locked when you borrow. You get it again when you repay. The important thing quantity to observe is your Mortgage-to-Worth (LTV) ratio, which determines how a lot you may borrow and what rate of interest you pay.

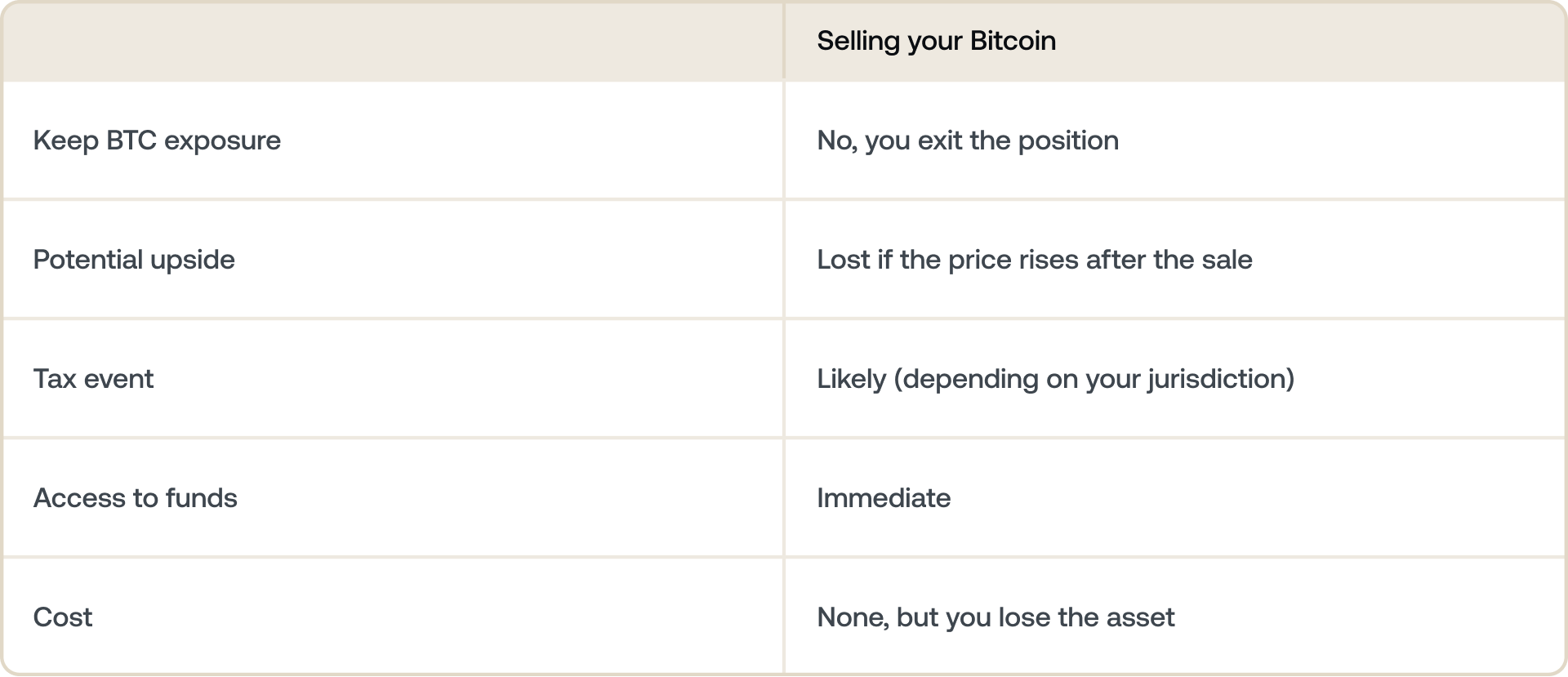

Promoting Bitcoin to cowl an expense seems like a trade-off you may't undo. If the worth goes up after you promote, you've got missed that upside, and relying on the place you reside, you might have triggered a taxable occasion too.

Borrowing towards your Bitcoin solves each issues. You entry liquidity at present whereas protecting your BTC precisely the place it's — working for you, probably appreciating, and never triggering a sale.

This information explains the way it works, what to be careful for, and the best way to do it with out taking over extra threat than you are comfy with.

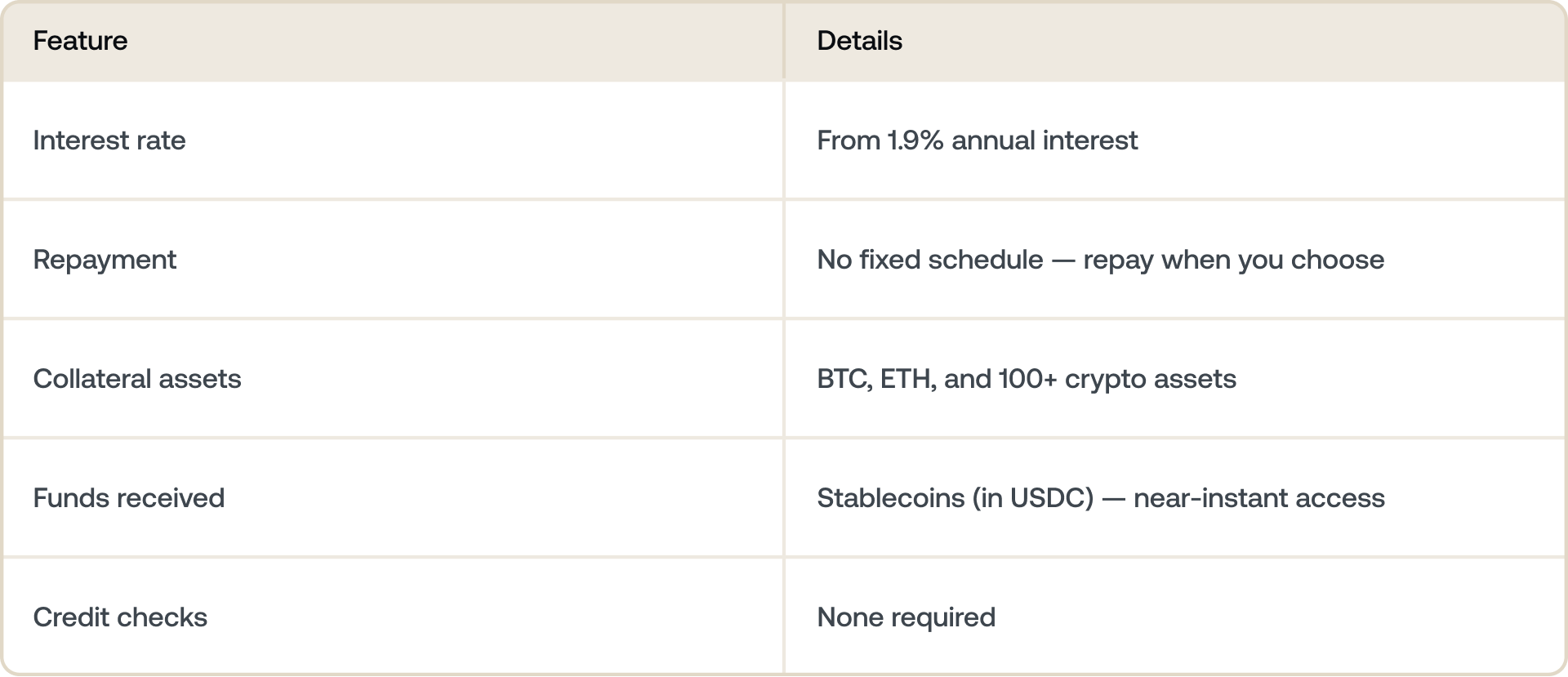

With Nexo's crypto-backed Credit score Line, you may borrow towards Bitcoin and different digital belongings at charges ranging from 1.9% annual curiosity — with no fastened compensation schedule and no credit score test. Discover how at nexo.com/borrow. Charges rely in your LTV and Loyalty Tier.

Why borrow towards Bitcoin as a substitute of promoting?

Rich traders have used this technique with actual property, shares, and artwork for many years. As an alternative of promoting an appreciating asset to fund a necessity, they borrow towards it. The asset retains rising. The mortgage will get repaid over time.

Bitcoin holders can now do the identical factor.

The trade-off is simple: borrowing prices cash (curiosity), however promoting prices you the longer term development of your Bitcoin. Which issues extra will depend on your view of the place BTC is heading and the way urgently you want the funds.

How borrowing towards Bitcoin works

The method is less complicated than most individuals count on. This is what occurs step-by-step.

You pledge your Bitcoin as collateral. This implies shopping for Bitcoin or including it to the platform. Your BTC is not bought — it is pledged as collateral for the mortgage.

You obtain funds. The platform provides you stablecoins — sometimes as much as 50% of your Bitcoin's present worth, relying in your chosen LTV.

Your BTC stays in your title. It is not bought or transferred away. If Bitcoin's value rises, you continue to profit from that enhance.

You repay at your tempo. Most crypto lending platforms do not impose a hard and fast compensation schedule. You repay when it fits you — in full or partly.

- Your Bitcoin is unlocked. As soon as you've got repaid the mortgage plus curiosity, your BTC is absolutely accessible to you once more.

An important idea: Mortgage-to-Worth (LTV)

LTV is the only most essential quantity in crypto-backed borrowing. Understanding it's important for you.

LTV is the ratio of what you borrow to what your collateral is value. For those who pledge $10,000 value of Bitcoin and borrow $5,000, your LTV is 50%.

What occurs when Bitcoin's value drops

That is the half that catches individuals off guard. Your LTV is not fastened — it strikes with the market.

Instance: You pledge 1 BTC value $100,000 and borrow $50,000 — a 50% LTV. If Bitcoin drops to $70,000, your LTV jumps to 71.4% ($50,000 / $70,000). If the liquidation threshold is 75%, you are now near having your collateral robotically bought. At all times borrow conservatively and monitor your LTV when the market is risky.

If Bitcoin drops in worth, the collateral backing your mortgage shrinks. Your LTV goes up robotically, even when you have not borrowed additional funds. If it crosses a platform's liquidation threshold, the platform could promote a few of your Bitcoin to convey the LTV again down.

How you can keep protected

- Set value alerts to your Bitcoin so you are not caught off guard.

- Solely borrow what you may repay comfortably, impartial of value actions.

How you can borrow towards Bitcoin on Nexo

Nexo's crypto-backed Credit score Line helps you to borrow towards Bitcoin and over 100 different belongings. This is what the expertise appears like in apply.

The rate of interest you pay will depend on your Loyalty Tier and your LTV. Nexo shoppers sustaining an LTV at or beneath 20% can entry an annual curiosity at 1.9%. See present charges and calculate how a lot you may borrow at nexo.com/borrow

What individuals really use crypto-backed loans for

Borrowing towards Bitcoin is not only a tax technique. Folks use it for a variety of sensible wants.

Masking bills with out promoting: House renovations, tuition, healthcare — excessive prices that may in any other case drive a sale at an inconvenient time.

Managing money circulation throughout volatility: If the market drops and you do not wish to promote at a loss, a short-term mortgage helps you to cowl fast wants whereas ready for circumstances to enhance.

Funding alternatives: Investing in a brand new enterprise, property, or asset with out liquidating a long-term crypto place.

- Retaining BTC publicity intact: Many long-term holders are reluctant to promote exactly as a result of they count on continued appreciation. A mortgage lets them entry worth with out giving up that potential.

Incessantly requested questions

1. Are you able to borrow towards Bitcoin?

Sure. You pledge your Bitcoin as collateral with a lending platform and obtain money or stablecoins in return. Your BTC is not bought — it stays yours and is unlocked when you repay the mortgage.

2. How a lot are you able to borrow towards Bitcoin?

It will depend on the platform and your chosen LTV. Most platforms can help you borrow as much as 50% of your Bitcoin's present worth. Borrowing much less — at a decrease LTV — provides you a bigger security buffer if Bitcoin's value drops, and sometimes provides you a decrease rate of interest on the crypto-backed mortgage.

3. What's LTV in a Bitcoin mortgage?

LTV stands for Mortgage-to-Worth. It is the ratio of your mortgage quantity to the worth of your collateral. For those who borrow $4,000 towards $10,000 of Bitcoin, your LTV is 40%. Your LTV strikes with Bitcoin's value — if the worth drops, your LTV rises, even when you have not modified the mortgage.

4. What occurs if Bitcoin drops whereas I've a mortgage?

Your LTV will increase robotically as your collateral loses worth. If it crosses the platform's liquidation threshold, the platform could promote a few of your Bitcoin to convey LTV again inside acceptable limits. The answer is to borrow conservatively — beginning at a low LTV provides you room to soak up value drops with out triggering liquidation.

5. Do you pay tax when borrowing towards Bitcoin?

In most jurisdictions, borrowing towards Bitcoin isn't a taxable occasion since you're not promoting or disposing of your BTC. The mortgage itself is not revenue. That mentioned, tax remedy varies by nation and particular person circumstances — seek the advice of a certified tax skilled for recommendation particular to your scenario.

6. Is borrowing towards Bitcoin protected?

It may be, in case you borrow conservatively and use a platform with institutional-grade custody. If Bitcoin's value drops far sufficient and quick sufficient, your collateral may be bought with out warning. Retaining a low LTV and monitoring your place throughout risky intervals considerably reduces that threat.

7. What is the distinction between a Bitcoin mortgage and a crypto credit score line?

The time period ‘credit score line' sometimes implies an ongoing facility the place you draw down funds as wanted and repay flexibly, reasonably than taking a single lump sum. Most crypto-native platforms supply a credit score line mannequin reasonably than a fixed-term mortgage.

These supplies are accessible globally, and the supply of this info doesn't represent entry to the providers described, which providers might not be accessible in sure jurisdictions. These supplies are for basic info functions solely and never supposed as monetary, authorized, tax, or funding recommendation, supply, solicitation, advice, or endorsement to make use of any of the Nexo Providers and will not be personalised, or in any approach tailor-made to mirror explicit funding aims, monetary scenario or wants. Digital belongings are topic to a excessive diploma of threat, together with however not restricted to risky market value dynamics, regulatory adjustments, and technological developments. The previous efficiency of digital belongings isn't a dependable indicator of future outcomes. Digital belongings will not be cash or authorized tender, will not be backed by the federal government or by a central financial institution, and most should not have any underlying belongings, income stream, or different supply of worth. Impartial judgment based mostly on private circumstances ought to be exercised, and session with a certified skilled is really useful earlier than making any resolution.